: Key Differences and How to Choose")

Decoding retirement financial savings is as thrilling as an all-day cram session for a standardized take a look at.

However similar to that grad faculty examination, your future kinda is dependent upon it.

401(okay)s and IRAs will be complicated — even to somebody who’s been writing about them for years — so I’m going to present you a simplified comparability that may provide help to resolve which to prioritize as you save for retirement.

Let’s have a look at the benefits and drawbacks of an employer-sponsored 401(okay) vs. a self-directed IRA.

What Is a 401(okay)?

A 401(okay) is a tax-advantaged retirement plan supplied by employers. Workers select a portion of their pretax wage to be deducted from every paycheck, which will probably be invested in property (usually mutual funds) chosen by the 401(okay)’s administrator. Contributions in a 401(okay) develop tax-free.

Employers usually incentivize workers to contribute to a 401(okay) by matching workers’ contributions, in full or partially.

What Is an IRA?

IRA stands for ‘particular person retirement account.’ IRAs differ from 401(okay)s in that they aren’t sponsored by an employer, and can be found to anybody with earned revenue.

Like a 401(okay), contributions to an IRA develop tax-free. However in contrast to a 401(okay), the contributions aren’t matched.

As a result of IRAs aren’t affiliated with a particular employer, buyers can select from numerous IRAs supplied by banks and brokers nationwide. An investor can even take a free hand in selecting which property to carry in an IRA.

Learn extra: Greatest IRA Accounts of 2022

Key Variations Between a 401(okay) and an IRA

| 401(okay) | IRA |

|---|---|

| Employer-sponsored account | Particular person account |

| Many employers at the very least partially match contributions | No contribution matches |

| Annual contribution restrict: $20,500 to $27,000 relying on age | Annual contribution restrict: $6,000 to $7,000 relying on age |

| Funding choices could also be restricted | Broad funding choices |

| Tax benefits range by account sort | Tax benefits range by account sort |

| Tough to keep away from early withdrawal penalties | Simpler to keep away from early withdrawal penalties |

Employer Matching

In case your employer provides a 401(okay), there’s likelihood they’ll match your contributions to a point. In different phrases, they’ll provide you with free cash for contributing to your 401(okay).

Now, how a lot they provide you varies considerably from one employer to the following. Many employers match as much as 50% of your contribution, capped at a certain quantity of your whole wage, like 3% or 6%. However it doesn’t matter what the match charge is, an employer’s contributions gained’t rely towards an worker’s annual 401(okay) contribution limits (see under).

As a result of IRAs are particular person plans slightly than employer-sponsored plans, there’s no equal alternative for a contribution match.

Contribution Limits

The entire level of 401(okay)s and IRAs is that Uncle Sam is providing you with a break in your taxes to encourage you to save lots of to your retirement. Sadly, there’s a restrict to this generosity.

In 2022, savers beneath age 50 can contribute as much as $20,500 to a 401(okay), however solely $6,000 to an IRA. These age 50 or older can even contribute additional ‘catch-up’ quantities of $6,500 and $1,000 yearly to 401(okay)s and IRAs respectively.

While you’re simply beginning out within the skilled world, contribution limits are hilarious. There’s no means most of us will come near them initially. However as you earn more cash, repay debt, and get severe about saving for retirement, it’s one other story.

For those who’re saving in an IRA solely, $6,000 in annual contributions probably gained’t be sufficient to completely fund the form of retirement you’re dreaming about. However a 401(okay)’s $20K+ annual restrict is loads of room for even probably the most aggressive savers, at the very least till you begin to critically advance in your profession.

Learn extra: How A lot Ought to You Save for Retirement?

Funding Choices

With an IRA, you possibly can spend money on just about something. You may have an IRA that merely holds a financial savings account, or an IRA with 100 completely different shares, bonds, ETFs, and mutual funds.

With a 401(okay), this often isn’t the case. Your employer usually companions with an exterior monetary providers firm to manage your plan. That firm then offers you a restricted variety of funding choices. Often, however not at all times, these are made up of mutual funds.

For those who work at a big firm you could have plenty of funding decisions inside your 401(okay). For those who work for a really small firm, nevertheless, it’s possible you’ll solely have 10.

For the typical Joe/Josephine, having fewer funding choices may really be a good factor. Most of us aren’t inventory pickers and shouldn’t attempt to be architects of the right portfolio with tons of of mutual funds.

That mentioned, extra skilled buyers may really feel restricted by the choices of their firm’s 401(okay), and may choose the liberty of an IRA. Moreover, mutual funds cost hidden administration charges, and a few 401(okay)s solely supply mutual funds with unnecessarily excessive charges that eat away at your funding returns.

Tax Benefits

Conventional 401(okay)s and IRAs

Usually, should you earn $500 and wish to make investments it in Apple inventory, you first need to pay revenue taxes in your earnings. So that you’d pay one thing like $100 of taxes and use the remaining $400 to purchase Apple shares. Assuming you maintain these shares for a few years, while you promote them, you’ll have to pay taxes on the quantity the shares have appreciated, referred to as capital beneficial properties tax.

With a conventional 401(okay), you don’t need to pay revenue tax on the cash you contribute. So on this circumstance, you’d earn $500 and make investments the complete $500.

Contributions to a conventional IRA will also be tax deductible, supplied neither you nor your partner have an employer-sponsored retirement plan as nicely, e.g., a 401(okay). For those who do have an employer-sponsored retirement plan, IRA contributions are solely totally tax deductible in case your annual revenue falls under a particular restrict ($68K for singles and $109K for married {couples} in 2022).

For each conventional 401(okay)s and IRAs, you’ll pay revenue tax on the cash you withdraw from the plans and/or on the necessary disbursements made out of the plans after you attain age 72. This taxation construction is advantageous to those that are at or close to the height of their skilled careers, and who count on to have decrease revenue of their retirement years.

Roth 401(okay)s and IRAs

Roth 401(okay)s and IRAs work otherwise, in that your contributions are taxed as common revenue, however your withdrawals in retirement aren’t taxed.

This taxation construction is advantageous to contributors who count on to have the next revenue of their retirement years than their present revenue, e.g., for individuals who are simply beginning out of their skilled careers.

The Roth IRA Property Planning Benefit

Roth IRAs are uncommon in that they are often handed right down to your heirs intact, and your heirs don’t need to pay taxes on the inheritance. That perk isn’t supplied with 401(okay)s or conventional IRAs.

Learn extra: Roth IRA or Conventional IRA — Which Ought to You Select?

Withdrawal Penalties

Right here’s the factor about retirement accounts: They’re meant for retirement.

Which means there are early withdrawal penalties.

For those who withdraw money from a conventional 401(okay) or IRA earlier than you flip 591/2, you’ll owe a ten% penalty on the withdrawal quantity to the IRS, on high of odd revenue taxes.

That mentioned, IRAs present a bit extra flexibility on this area, and there are a selection of exceptions to the IRA early withdrawal penalty. You may, for instance, use penalty-free withdrawals to cowl increased training bills and as much as $10,000 towards the acquisition of your first dwelling (or any dwelling, supplied you haven’t been a house owner for the earlier two years).

A Roth IRA is much more versatile, in you could make penalty-free withdrawals from it at any age and for any purpose as much as the quantity of your whole contributions (not together with earnings/progress inside the account).

Against this, with a 401(okay) you need to show extreme monetary hardship to acquire an exemption from the early withdrawal penalty.

Some employers, nevertheless, permit you to take out a 401(okay) mortgage. Primarily, you borrow cash from your self. Though this feels like an amazing thought, it’s a slippery slope. Any cash you borrow ceases to earn returns for you and, should you lose your job, you need to repay the whole mortgage or pay revenue taxes and the ten% penalty on the excellent stability.

Learn extra: Can I Ever Money Out My 401(okay)?

Professionals and Cons of a 401(okay)

Professionals Cons

- Excessive contribution limits

- Employers may match contributions

- Computerized retirement financial savings

- Appropriate for all ranges of funding information

- Provided to workers solely

- Restricted alternative of investments

- Might cost excessive charges

- Arduous to keep away from penalties on early withdrawals

Professionals and Cons of an IRA

Professionals Cons

- Accessible to just about anybody

- Big selection of doable investments

- Simpler to seek out low-fee choices

- Gives extra loopholes for penalty-free withdrawals

- Roth IRAs will be transferred to heirs tax-free

- Low contribution limits

- No contribution matching

- Requires extra funding information

FAQs

Is a 401(okay) an IRA?

A 401(okay) just isn’t the identical factor as an IRA. Each are forms of retirement accounts, however they differ in a couple of key methods. A very powerful distinction is that 401(okay)s are supplied by employers, whereas IRAs can be found to anybody who has earned revenue.

Can You Lose Cash in a 401(okay) or IRA?

The property held in 401(okay)s and IRAs can rise or fall in worth because the market fluctuates, so, sure you possibly can lose cash in both a 401(okay) or IRA.

However correctly diversified portfolios are more likely to respect in worth over time. And you may regulate your 401(okay) or IRA’s asset allocation to match your danger tolerance.

Can I Put Off Saving for Retirement?

Sometime your will to work will disappear. Your payments, sadly, gained’t.

So, in most circumstances, no, you possibly can’t postpone saving for retirement. And the longer you set it off the much less you’ll reap the advantages of compound curiosity.

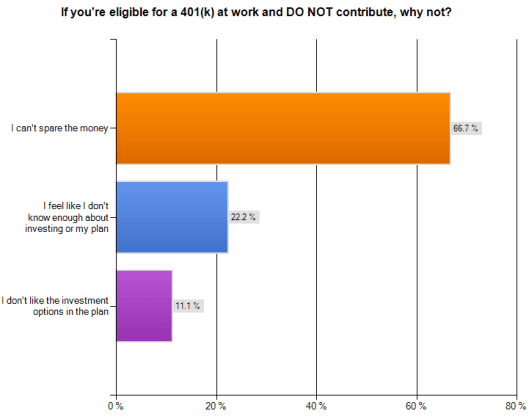

No matter excuse you’ve for not saving for retirement most likely falls into a number of of the under three classes.

Now, let’s debunk a few of these widespread excuses one after the other:

Sure, You Can Spare at Least Some Cash for Retirement

It’s onerous to set cash apart when Two-Buck Chuck is your go-to drink and your iPhone remains to be in your dad or mum’s household plan. I completely empathize with that.

However even should you can solely contribute 1% of your paycheck to a retirement plan, at the very least that’s one thing.

What’s most essential is that you just:

- Take the cash you possibly can spare and routinely make investments it into both a 401(okay) or IRA.

- Attempt to max out your employer’s 401(okay) match.

- For those who’re not an worker, make investments no matter it can save you in a balanced IRA portfolio of shares and bonds. Don’t create an IRA comprised of low-risk investments, like CDs.

Learn extra: How Investing Simply $50 a Month Can Kickstart Your Retirement

I’m Not Educated Sufficient to Make investments

No drawback! You may nonetheless save for retirement when you steadily enhance your investing savvy.

The oldsters managing your organization’s 401(okay) are educated sufficient to take a position your cash for you. And should you don’t have a 401(okay), a lot of the high robo-advisors at present supply IRAs.

My Firm’s 401(okay) Is Underwhelming

That’s positively a bummer, however not an excuse to keep away from investing for retirement.

For those who’re savvy sufficient to comprehend that there are higher choices on the market than your organization’s 401(okay), you’re most likely savvy sufficient to open your personal IRA and take private management of your investments.

I Have Excessive-Curiosity Debt

Okay, you discovered one in every of solely two justifiable excuses not to save lots of for retirement. At the least not but.

While you’re paying 10% or extra in curiosity on bank card debt, you must direct no matter cash you save every month towards repaying your card stability.

However when you’ve paid that debt off, it’s time to contribute aggressively to your retirement plan! Take no matter earnings you had been allocating towards debt repayments and contribute them to your 401(okay) or IRA as a substitute.

Learn extra: Ought to You Delay Retirement Contributions to Pay Off Debt?

I Don’t Have an Emergency Fund

It’s a good suggestion to steadily save up a wholesome emergency fund earlier than you begin specializing in saving for retirement. Divert a part of every paycheck till you’ve three months to at least one 12 months’s value of financial savings accrued in an interest-bearing however liquid account, like a high-yield financial savings account. You should use an emergency fund calculator should you’re undecided what number of months’ bills you must save.

As soon as your emergency fund is full, you already know the drill: Shift focus and contribute the month-to-month sum you previously deposited into your emergency fund into your 401(okay) or IRA as a substitute.

Abstract: Is It Higher to Have a 401(okay) or IRA?

For these eligible, 401(okay)s are positively the best technique to save for retirement. The cash is routinely taken out of your paycheck, and the restricted alternative of investments can really be factor, because it simplifies your decision-making course of.

The 401(okay) employer match can be a significant draw. Over time employer match can really permit you to retire years sooner than you’d have in any other case.

These concerns probably make the 401(okay) one of the best retirement automobile for most of our readers.

That mentioned, there’s no scarcity of freelancers on the market that don’t have entry to a 401(okay). And most younger professionals stand to learn extra from an IRA’s tax benefits, which favor lower-income contributors.

For those who fall into greater than one of many above classes, e.g., you’ve entry to an employer-sponsored 401(okay) however you haven’t reached your peak incomes years, think about the next traditional strategy to retirement saving:

- Contribute sufficient to your employer’s 401(okay) so that you just max out their contribution match.

- Make investments any remaining cash it can save you into an IRA.

- Rinse and repeat till your revenue is excessive sufficient you could hit the contribution limits for each a 401(okay) and an IRA.

Learn extra: